2025 Canadian Pension Climate Report Card

A tale of two pension managers

The following forms part of Shift’s 2025 Canadian Pension Climate Report Card, using publicly available data to December 31, 2025. Find the full CPPIB analysis here, and the full La Caisse analysis here.

The growing divide between forward-looking and backward-looking economies is reflected in the gulf between Canada’s two largest pension managers. The Canada Pension Plan Investment Board (CPPIB) and the Caisse de dépôt et placement du Québec (formerly CDPQ, now La Caisse) are taking dramatically different approaches to the climate crisis.

CPPIB, which manages more than $777 billion on behalf of over 22 million Canadians, quietly abandoned its net-zero commitment in May 2025. Shift had questioned the credibility of this commitment in previous report cards, as CPPIB refused to set interim targets and continued to invest in fossil fuel expansion. CPPIB itself may have felt that the credibility of its net-zero commitment might not stand up to scrutiny – when it dropped the target, it cited “recent legal developments in Canada”. This was almost certainly a reference to Bill C-59’s provisions to combat false, misleading, or unsupported environmental claims. Perhaps for the same reason, the fund appears to have jettisoned its commitment to invest $130 billion in “green and transition assets” by 2030.

Canada’s largest pension manager went on to commit at least $7.1 billion in pension capital to new oil, gas, coal and pipeline assets from October 2024 to October 2025 while also seeming to go out of its way to bolster the fossil fuel industry. In July 2025, CPPIB proudly highlighted its decade of investment in Canada’s largest oil and gas producer, Canadian Natural Resources Limited (CNRL), praising its “long-term production stability”. In September 2025, CEO John Graham said “Here in Canada, we like pipelines. We like oil and gas pipelines. We have Wolf Midstream (Inc.) in Alberta.” CPPIB-owned Wolf’s business model relies on increasing greenhouse gas emissions and locking in high-risk fossil fuel dependence, while the fund’s investments in CNRL have positioned the company to increase production. The success of these companies jeopardizes the stability of the climate, which is foundational to CPPIB’s ability to generate long-term returns.

CPPIB no longer appears to have a publicly-disclosed climate strategy, and its 2025 climate-related financial disclosures severely underestimated how a “hot-house” climate scenario could harm its ability to fulfill its mandate, an issue that Shift raised in a letter to Canada’s Office of the Chief Actuary. CPPIB ends 2025 facing a lawsuit over its handling of climate-related risk, while ranking second-lowest overall in Shift’s report card.

Hirji et al v. Canada Pension Plan Investment Board

In October 2025, four young Canadians (the applicants) launched legal proceedings against CPPIB, which manages the Canada Pension Plan (CPP). They allege that CPPIB is failing to protect their future pensions from the financial risks posed by climate change. The applicants are being represented by Canadian environmental law charity Ecojustice and employment, labour and pensions law firm Goldblatt Partners LLP.

The applicants, born after 1990 and ineligible for CPP benefits until after 2050, are concerned about the impact of climate change on their long-term financial security. As newer entrants to the workforce, they will retire in a world shaped by today’s investment decisions. The case argues that CPPIB’s mismanagement of climate-related risks threatens the stability of the pension fund and the retirement security of young Canadians, who will bear the long-term consequences of climate change.

The applicants allege that CPPIB has a duty to make investment decisions that align with their best interests – which include a stable financial system, healthy economy, and livable climate. They claim that CPPIB is failing to adequately identify, assess and manage climate-related financial risks while continuing to invest billions of dollars in oil, gas and coal – the primary drivers of the climate crisis.

The case argues that CPPIB’s responsibilities require the investment manager to:

- Recognize climate change as a systemic financial risk, and manage it prudently and responsibly;

- Acknowledge that fossil fuel investments exacerbate climate change, expose the CPP portfolio to increased risk of loss and to unacceptable stranded asset risk, and ultimately destabilize the global economy and financial system upon which pension funds depend;

- Protect the long-term stability of the pension fund; and

- Invest responsibly today to ensure a secure retirement for generations to come.

The applicants are not seeking monetary compensation. Rather, they are asking the court to order declaratory relief to recognize CPPIB’s legal duty to act in the best interests of pension contributors and future retirees by credibly addressing climate-related financial risks.

For more information about the climate litigation against CPPIB, click here.

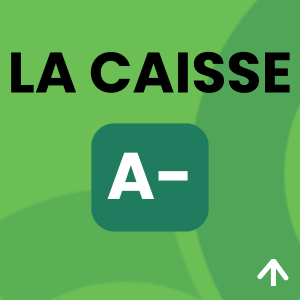

In stark contrast, CPPIB’s Quebec counterpart has pursued a far more ambitious path on climate. La Caisse, which manages more than $496 billion on behalf of 6 million Quebecers, has shown an understanding of systemic risk, the pace of the energy transition, and its obligations to beneficiaries and contributors. The investment manager has set climate targets early, achieved them, and then followed up with more ambitious targets. In 2025, having reduced its portfolio emissions intensity by 69% from 2017 levels and completed its exit from coal and oil production, La Caisse launched a new climate strategy that focuses on decarbonizing the real economy. The investment manager pledged $400 billion to “climate action” by 2030, and coupled the strategy with a transition financing framework anchored in credible international standards.

La Caisse explicitly placed sustainable investing “at the heart of [its] fiduciary responsibility”, cited the international goal of limiting global heating to 1.5°C, and warned of the world being off course. The fund’s transition financing framework referenced the Paris Agreement and Paris alignment throughout, cited the International Energy Agency’s expectation that demand for coal, oil and gas will likely peak this decade, and noted that “the transition and the accelerating decarbonization of the economy are generating investment opportunities that are significant, promising and profitable.”

With this year’s overall A minus, La Caisse becomes the first Canadian pension manager to receive an overall A-range grade in any of Shift’s report cards – going back to 2022. However, La Caisse must not jeopardize its climate-leading reputation: it must disclose credible, profitable, science-based transition plans for its gas distribution and transmission assets in Quebec, the United States and Brazil, or else remove these assets from its portfolio.

Climate action at La Caisse

La Caisse’s climate strategy and transition financing framework were a shining light in a year in which climate progress was threatened.

The Quebec investment manager laid out categories for its pledged $400 billion in “climate action” investments – a number so large that it will influence decisions made across every investment team at La Caisse. The $400 billion will consist of “climate solutions” investments and “decarbonization” investments. Investments in “climate solutions” must qualify for one of four categories: low-carbon assets, nature-based solutions, adaptation and resilience solutions, and “enablers”. Crucially, the definition for each climate solutions category is grounded in credible frameworks. La Caisse’s tiered system of “decarbonization” investments suggests an intent to help companies progress from “committed” to “aligned” to “fully aligned”, but does not spell out a timeline for alignment, nor does it explicitly rule out fossil fuel investments. La Caisse’s use of the “Do No Significant Harm” principle acts as a necessary backstop: it “aims to prevent investments from unintentionally locking-in high-emission activities, undermining decarbonization goals or causing significant harm to other environmental and social objectives.”

The transition financing framework as a whole earned the endorsement of the Climate Bonds Initiative, while elements within it anchored La Caisse’s commitments to methodologies including the Science Based Targets initiative, Net Zero Investment Framework, Transition Pathway Initiative (now being integrated into the International Sustainability Standards Board framework) and Net-Zero Asset Owner Alliance (NZAOA).

Stakeholders have yet to see how La Caisse will implement its new strategy and report on progress. But the investment manager’s consistent climate leadership – which has included setting carbon reduction targets for each of its portfolios in 2017, linking staff compensation to climate targets since 2018, co-founding the NZAOA, placing exclusions on coal and oil, and transparent reporting on its “transition envelope” – provides a strong indication that the investment manager is equipped to follow through.

As La Caisse wrote in the transition financing framework, “The success of our approach will be measured in terms of exposure to climate action investments in billions of dollars.”

The 2025 Canadian Pension Climate Report Card analyses, assesses and ranks the progress made by eleven of Canada’s largest pension managers and two international pension managers in their approach to climate risk and investment decisions as they relate to the climate crisis. The report is based on publicly available information to December 31, 2025. Cover image credit: Jim Peaco / National Park Service.

View another pension fund manager